Minimum Credit Score Needed to Buy a House: 7 Powerful Facts Every Buyer Must Know

Understanding the Minimum Credit Score Needed to Buy a House

Buying property often requires financing through a mortgage lender. One of the first things lenders review is your credit score.

The Minimum Credit Score Needed to Buy a House depends largely on the type of mortgage you apply for and the lender’s requirements. Generally, most lenders look for a score between 580 and 620, though some programs allow lower scores under special circumstances.

What Is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness. It shows lenders how likely you are to repay borrowed money.

Credit scores typically range from 300 to 850 and are based on several factors:

-

Payment history

-

Credit utilization

-

Length of credit history

-

Types of credit accounts

-

Recent credit inquiries

The higher your score, the lower the risk for lenders.

Why Mortgage Lenders Check Your Credit

Mortgage lenders review your credit report to determine:

-

Your ability to repay a loan

-

Your history of managing debt

-

Your reliability as a borrower

A strong credit profile helps lenders feel confident approving your mortgage application.

How Credit Scores Impact Mortgage Approval

Your credit score affects several important factors:

-

Mortgage approval

-

Interest rates

-

Down payment requirements

-

Loan options available

Even a small increase in your score can save thousands of dollars over the life of a mortgage.

Minimum Credit Score Needed to Buy a House for Different Loan Types

Different mortgage programs have different credit score requirements. Understanding these options helps buyers choose the best loan for their situation.

Conventional loans are not backed by the government.

Typical requirements include:

-

Minimum credit score: 620

-

Stable income

-

Low debt-to-income ratio

Borrowers with scores above 740 usually receive the best interest rates.

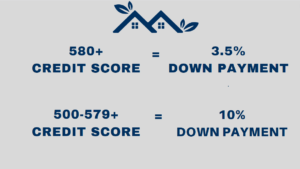

FHA loans are popular among first-time homebuyers because they have more flexible credit requirements.

Typical FHA credit score requirements:

-

580 for a 3.5% down payment

-

500–579 with a 10% down payment

These loans are insured by the Federal Housing Administration and are designed to help more people become homeowners.

You can learn more about FHA programs on the official U.S. Department of Housing and Urban Development website:

https://www.hud.gov

VA loans are available to eligible veterans, active-duty military members, and certain spouses.

Benefits include:

-

No down payment

-

No private mortgage insurance

-

Competitive interest rates

A minimum credit score of 500 is required for VA loans.

USDA loans help buyers purchase homes in eligible rural areas.

Typical requirements:

-

Credit score as low as 550

-

Moderate income limits

-

Property located in a USDA-approved area

These loans often offer zero down payment options.

How Credit Score Affects Mortgage Interest Rates

Your credit score doesn’t just determine eligibility. It also impacts how much you pay in interest.

Credit Score Tiers

Lenders usually categorize credit scores into tiers:

Credit Score

|

Rating |

|---|---|

760–850 |

Excellent |

700–759 |

Very Good |

660–699 |

Good |

620–659 |

Fair |

580–619 |

Poor |

Higher tiers typically receive lower mortgage interest rates.

Example Rate Differences

Consider a $300,000 mortgage:

Credit Score

|

Estimated Interest Rate |

Monthly Payment |

|---|---|---|

760+ |

6.0% |

$1,799 |

680 |

6.5% |

$1,896 |

620 |

7.2% |

$2,037 |

Over 30 years, a higher credit score could save tens of thousands of dollars.

Other Factors Lenders Consider Besides Credit Score

While the Minimum Credit Score Needed to Buy a House is important, lenders evaluate other financial factors as well.

Debt-to-Income Ratio

Your debt-to-income (DTI) ratio measures how much of your monthly income goes toward debt payments.

Most lenders prefer:

-

DTI below 43%

Lower ratios improve approval chances.

Employment History

Stable employment shows lenders that you have consistent income.

Typical requirements include:

-

Two years of steady work history

-

Reliable income documentation

Down Payment Size

A larger down payment reduces risk for lenders.

Benefits of higher down payments:

-

Lower monthly payments

-

Better interest rates

-

Increased approval odds

Tips to Improve Your Credit Score Before Buying a Home

If your credit score is below the recommended level, there are several ways to improve it before applying for a mortgage.

Pay Bills on Time

Payment history accounts for about 35% of your credit score.

Consistent, on-time payments can significantly boost your score over time.

Reduce Credit Card Balances

Keep your credit utilization below 30% of your credit limit.

For example:

-

Credit limit: $10,000

-

Ideal balance: $3,000 or less

Lower balances signal responsible credit management.

Avoid New Credit Applications

Opening new credit accounts before applying for a mortgage can temporarily lower your score.

It’s best to avoid:

-

New credit cards

-

Auto loans

-

Personal loans

during the mortgage approval process.

Can You Buy a House With Bad Credit?

Yes, buying a home with bad credit is possible.

While it may be more challenging, many programs exist to help borrowers with lower scores.

Options for Low Credit Borrowers

Possible strategies include:

-

FHA loans

-

Larger down payments

-

Co-signers

-

Credit repair programs

Government Loan Programs

Government-backed loans often have more flexible credit requirements and can help first-time buyers qualify more easily.

Step-by-Step Guide to Preparing for a Mortgage

If you want to qualify for a home loan, preparation is key.

Check Your Credit Report

Before applying for a mortgage:

-

Review your credit report

-

Dispute errors

-

Identify areas for improvement

Save for a Down Payment

While some loans require little or no down payment, saving more money upfront can strengthen your application.

Get Pre-Approved

Mortgage pre-approval helps buyers:

-

Understand their budget

-

Show sellers they are serious

-

Speed up the home buying process

Common Mistakes First-Time Homebuyers Make

Avoiding common mistakes can make the home buying journey much smoother.

Ignoring Credit Reports

Many buyers fail to review their credit reports before applying for a mortgage.

This can lead to surprises that delay approval.

Taking on New Debt

Large purchases—such as cars or furniture—can increase your debt and hurt your chances of mortgage approval.

FAQs About Minimum Credit Score Needed to Buy a House

1. What is the minimum credit score needed to buy a house?

The Minimum Credit Score Needed to Buy a House typically ranges from 500 to 620, depending on the loan program.

2. Can I buy a house with a 500 credit score?

Yes, some FHA loans allow scores as low as 500, but they require a 10% down payment.

3. What credit score is needed for the best mortgage rates?

Most lenders offer the best rates to borrowers with scores 740 or higher.

4. Does checking my credit hurt my score?

Soft credit checks do not affect your score. Hard inquiries from lenders may cause a small temporary drop.

5. How long does it take to improve a credit score?

Depending on the situation, noticeable improvements can take 1 to 12 months.

6. Can first-time homebuyer programs help with low credit?

Yes. Many first-time buyer programs offer flexible credit requirements and down payment assistance.

Conclusion to Minimum Credit Score Needed to Buy a House

Understanding the Minimum Credit Score Needed to Buy a House is essential for anyone planning to purchase a home. While many lenders prefer scores above 620, several loan programs allow buyers with lower scores to qualify.

Improving your credit score, reducing debt, and saving for a down payment can dramatically increase your chances of approval. With careful preparation and the right loan program, homeownership may be closer than you think.

Buying a home is a significant financial step, but with the right knowledge and planning, it can become one of the most rewarding investments you’ll ever make.

Apply Now!

For a quicker response, call 888-958-5382

Mortgage-World

Written by: Chris Luis, owner/loan officer for Mortgage-World.com

-

Chris Luis covers mortgages and the housing market. He has over 20 years experience in the mortgage industry.