Mortgage Insurance

Mortgage Insurance

When you’re planning to buy a home, there’s a good chance you’ll hear the term mortgage insurance. It may sound like just another added cost, but understanding what it is—and why it exists—is crucial. So, let’s break it down in a way that actually makes sense.

Mortgage insurance (MI) is a policy that protects the lender, not you as the borrower. Wait, what? Yup, that’s right. Even though you’re the one paying for it, the benefits go directly to the lender. It’s designed to minimize the lender’s risk in case you default on your mortgage payments. This insurance becomes especially important when you’re putting down less than 20% of the home’s purchase price.

For lenders, low down payments mean high risk. MI is their backup plan, giving them a safety net. For you, it’s kind of a double-edged sword—it helps you get into a home with a smaller upfront cost, but adds to your monthly expenses.

Let’s say you’ve got your eye on a $300,000 house, but you only have $15,000 saved up for a down payment. That’s 5%, far less than the traditional 20% many lenders prefer. So, how do you convince them you’re worth the risk?

Enter mortgage insurance.

The purpose here is simple: protect the lender from loss if you fail to make your mortgage payments. Without it, most banks would flat-out reject low down payment borrowers. So in a way, mortgage insurance opens doors that would otherwise remain locked for first-time buyers or anyone with limited savings.

The lender takes comfort in knowing they’ll get reimbursed—even partially—if things go south. You, on the other hand, get your foot in the door without needing to save up tens of thousands more.

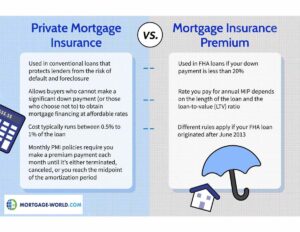

Typically, if your down payment is less than 20% on a conventional loan, you’re required to carry mortgage insurance. However, the rules vary depending on the loan type.

Conventional Loans: Less than 20% down? PMI is likely required.

FHA Loans: MIP is mandatory, regardless of the down payment amount.

VA Loans: No mortgage insurance required—but more on that later.

Even if you’re a high-income earner with great credit, a small down payment means you’re still seen as a higher-risk borrower. So yes, MI doesn’t discriminate—it’s all about percentages, not people.

This is the most common form and usually applies to conventional loans. PMI can be paid monthly, upfront, or both. Rates depend on several factors, like your credit score, loan amount, and loan-to-value ratio (LTV).

Here’s how PMI works:

Monthly Premiums: Added to your mortgage payment.

Upfront Premium: Paid at closing but reduces your monthly cost.

Split Premium: Combines both to balance affordability.

PMI isn’t forever, though. Once your loan balance drops to 78% of the home’s original value, it typically goes away automatically.

If you’re using an FHA loan, you’re dealing with MIP. Unlike PMI, MIP sticks around longer and comes with both upfront and annual payments.

Key features of MIP:

Upfront Cost: Typically 1.75% of the loan amount.

Annual Premium: Divided monthly across your payments.

Duration: Often required for the life of the loan unless you refinance.

The rules are a bit stricter here, so while FHA loans are easier to qualify for, MIP is one of the trade-offs.

With LPMI, the lender pays your insurance—but wait, don’t get too excited. They’re not doing it out of generosity.

Instead, they roll the cost into your loan, meaning you’ll pay a slightly higher interest rate for the life of your mortgage. This can be a good option if you plan to sell or refinance in a few years, but it’s usually more expensive over the long run.

Here’s a general rule of thumb: If your down payment is under 20%, you’re probably going to need mortgage insurance.

But it also depends on:

The type of mortgage

The loan-to-value (LTV) ratio

Your credit score

The lender’s internal policies

Some lenders might still require it even with 20% down if your credit is less than stellar. The goal is always to offset their potential risk.

Several factors go into the cost of mortgage insurance:

Loan Amount: Bigger loan = bigger risk.

Credit Score: Lower scores mean higher premiums.

LTV Ratio: The closer you are to 100% loan, the higher the cost.

Loan Term: Shorter terms may have slightly lower premiums.

On average, PMI costs about 0.5% to 1.5% of the loan amount annually. So on a $300,000 mortgage, that could be $1,500 to $4,500 per year—or $125 to $375 monthly.

MIP for FHA loans is generally more predictable but less flexible in terms of cancellation.

The good news? Mortgage insurance doesn’t last forever—at least not always.

PMI: Usually drops off automatically at 78% LTV or can be requested at 80%.

MIP: Stays for at least 11 years, often for the life of the loan unless refinanced.

LPMI: Embedded in the loan via higher interest; can’t be removed.

So knowing when and how it ends can help you plan for refinancing or making extra payments to speed things up.

Mortgage-World